Running a small business in Florida feels like juggling sunshine, customers, invoices, and… paperwork that sometimes looks like it’s written in another language. You know that moment when you’re going through your books at midnight, and one number feels “off,” but you can’t explain why?

That’s where the trial balance quietly saves the day. It’s not fancy. Not dramatic. But it keeps your books steady, clean, and ready for tax time.

And honestly, once you understand how it works, you’ll wonder why nobody teaches this in school.

Before anything else, let’s answer the big question many business owners ask without saying it out loud: what is a trial balance?

Because once that’s clear, everything else clicks.

What Is a Trial Balance and Why It Still Matters?

A trial balance is a simple accounting report that lists all your ledger accounts along with their ending debit or credit balances. If everything in your books was recorded correctly, the total debits will match the total credits.

And you know what? When those totals match, it feels strangely satisfying, like closing all the open tabs on your browser after a long week.

So, what is a trial balance really telling you?

It’s saying:

“Your numbers might not be perfect, but at least they are mathematically balanced.”

This matters more than most business owners imagine. When you’re getting ready for tax time or preparing documents to show the IRS during filing, having your books balanced can prevent a lot of stress.

Speaking of the IRS, if you’re filing taxes or preparing financial statements, their official guidance on records can be found here:

IRS Recordkeeping Requirements

You don’t need to study it deeply, but it’s helpful to know the source.

The Real Purpose Behind a Trial Balance

Here’s the thing: a trial balance isn’t just about neat math. It’s about peace of mind.

It helps you spot mistakes early, before they turn into bigger issues like misstated income or missing expenses. One small mistake in your ledger can snowball into IRS letters, late fees, or incorrect tax returns. This report acts like a friendly warning system.

If bookkeeping still feels overwhelming, you’re not alone. Most Florida owners don’t have time to sit with spreadsheets after a full day of running their shop, salon, landscaping crew, or even managing Florida cleaning businesses. That’s why tools like our simple bookkeeping plan can help lighten the load. Many owners also rely on our professional business bookkeeping services to keep their books organized all year.

Sometimes, paying a little for help saves a lot in the long run.

Ledger and Trial Balance — How They Work Together

You can’t understand the ledger and trial balance relationship without thinking of it like a kitchen.

The ledger is the recipe, the list of every single ingredient (transaction).

The trial balance is you checking the ingredients on the counter before you cook, making sure you didn’t forget the salt or double the sugar.

Every transaction you enter into your books flows into your ledger. Then your ledger balances flow into the trial balance. Simple. Clean. Natural.

And if you’re using a software like QuickBooks, Xero, or Wave, it does this quietly in the background. But even then, you should still check your trial balance monthly to spot mistakes before they cost you.

Trial Balance Format — What It Looks Like in Real Life

Even if accounting isn’t your thing, easy to follow.

It usually includes:

- Account Name

- Debit Balance

- Credit Balance

- Total Debit and Total Credit at the bottom

That’s it. No complicated formulas. No deep financial theory.

It’s simply a list that should balance.

And when it doesn’t, you know something somewhere went sideways.

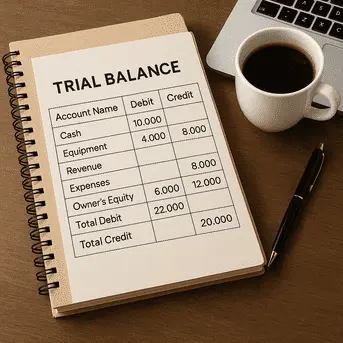

A Simple Trial Balance Example You Can Picture

Let’s imagine a small Florida landscaping business.

Account Name — Debit — Credit

- Cash: $10,000 debit

- Equipment: $4,000 debit

- Revenue: $8,000 credit

- Expenses: $6,000 debit

- Owner’s Equity: $12,000 credit

Total Debits = $20,000

Total Credits = $20,000

Boom. Balanced.

When you see it like this, the concept a becomes much clearer.

Common Errors a Trial Balance Helps You Catch

Even the best business owners make mistakes. And honestly, the better the business, the faster the bookkeeping errors happen because you’re busy with real work.

A trial balance helps catch errors like:

- Posting something twice

- Missing an entry completely

- Reversing debit and credit

- Typing an extra zero

- Forgetting to close out a temporary account

- Bank errors that slip by without noticing

You know what’s funny? Many owners think accounting software eliminates errors. It doesn’t. It just hides them better. The trial balance is still necessary, like checking your tire pressure even if your car is modern.

How Florida Small Businesses Actually Use a Trial Balance

Some business owners review their trial balance monthly. Others wait until tax season and then pray everything matches. But in Florida, with seasonal highs and lows, it’s especially important to know where your money is going.

Here’s how local businesses usually use it:

- For end-of-year taxes: A clean trial balance reduces the chance of IRS adjustments.

- For monthly planning: Know if your expenses are creeping up. You can also review unpaid invoices using our accounts receivable guide

- For loans or credit: Banks love clean records.

- For growth: You can’t scale without knowing where you stand financially.

And let’s be honest, most Florida businesses deal with unpredictable months. Hurricanes, heat waves, snowbirds leaving… your numbers can change fast. The trial balance keeps you steady through the swings.

Trial Balance vs Financial Statements — Don’t Mix Them Up

You might think the trial balance and the financial statements are the same thing. They’re not. If you want to understand margins better, check this helpful contribution format income statement.

- Trial balance: Internal check for accuracy

- Financial statements: External documents for bank loans, investors, the IRS, or your personal understanding

Think of the trial balance as the rehearsal. The financial statements are the show.

Your ledger and trial balance work together to feed the final performance.

Modern Tools That Make Your Trial Balance Easier

You don’t have to do everything manually. Modern accounting tools automate a lot, but they still depend on correct input. Garbage in = garbage out.

Helpful tools include:

- QuickBooks Online

- Xero

- Wave

- FreshBooks

- Zoho Books

These tools generate the trial balance in one click. But they can’t catch mistakes you forgot to enter. That’s why reviewing it monthly helps you keep your books healthy.

If you want a simple plan to keep things organized, our Bookkeeping Lite service can help

Step-by-Step: How to Prepare a Trial Balance Without Stress

Relax. Grab a cup of coffee. Let’s walk through it.

- Gather all ledger balances

Every account should have an ending balance. - Separate debit and credit amounts

This keeps everything visually clear. - List each account

Keep it tidy—your future self will thank you. - Add up the debits

Write the total at the bottom. - Add up the credits

Write that total too. - Compare the totals

Do they match?

If they don’t, don’t panic. It happens to everyone, even accountants who’ve been doing this for 20 years.

This checklist also shows how the ledger and trial balance system works together.

When Your Trial Balance Doesn’t Balance — Here’s What to Do

If your trial balance refuses to balance, don’t jump to the worst conclusion. It usually means one of these:

- A transaction was left out

- Something was posted on the wrong side

- A number was typed incorrectly

- The ledger totals are off

- A temporary account isn’t closed

- A beginning balance was entered incorrectly. And if your books are already messy, our bookkeeping clean-up services can fix them quickly.

Here’s a trick accountants use:

Start checking the areas with the biggest numbers first. Problems often hide there.

Another trick:

Check anything recorded at 10pm when you were tired. Those entries cause chaos.

Do You Still Need a Trial Balance If Software Does Everything?

Short answer: Yes.

Long answer: Absolutely yes.

Software automates things, but the IRS still holds you responsible for accuracy. If your numbers are off, even by accident, the IRS doesn’t care if QuickBooks did it or if your neighbor’s cousin helped you.

Checking your trial balance monthly gives you control, clarity, and fewer surprises during tax season.

You can read the IRS explanation of why accurate bookkeeping matters here

Even they emphasize keeping clean books.

Final Thoughts: Why a Trial Balance Keeps Your Business Calm and Clean

Running a business in Florida isn’t always calm. You’ve got seasons, storms, taxes, customers, staff, supplies, and everything in between. Your numbers shouldn’t be another source of stress.

The trial balance is simple, quiet, and old-school, but it continues to play a crucial role in keeping your finances steady.

If you want help keeping your monthly bookkeeping clean and ready for tax season, check out our simple plan

A clean business is a strong business. And a balanced trial balance is one of the cleanest places to start.