Filling out a check for business transactions is still an important skill. Even with electronic payments on the rise, checks continue to play an essential role in commercial payments.

Writing a check correctly ensures your payments are accurate, reduces errors, and helps you keep detailed records. Check out this guide for step-by-step instructions on how to write a check and the common mistakes to avoid.

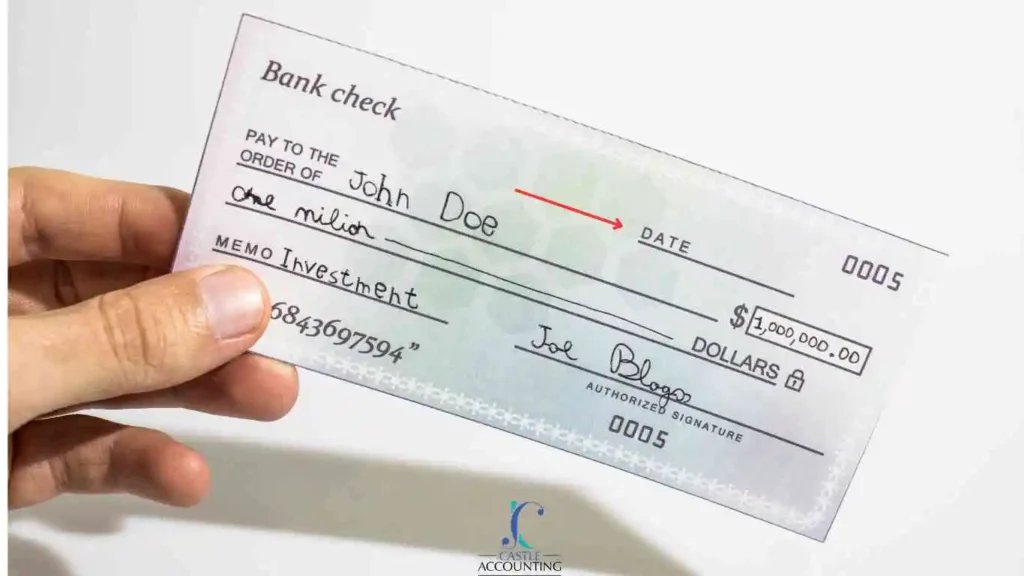

How to write a check step by step

1. The Date

The date line is at the top right of the check. Write the current date clearly to avoid confusion. Accurate dates are essential for tracking payments and ensuring checks don’t expire.

2. Pay to the Order of

This is simply the name of the person or business receiving the money. You’ll usually see it written on the check.In a check example: if the payment is going to John Doe, the check will clearly list John Doe as the payee.

3. Amount in Numbers

The amount in numbers prevents discrepancies and reduces the chance of fraud. Typically, the amount is written to the right of “Pay to the Order of” in a designated box.

For instance, $1,000,000.00 should be written as “1,000,000.00.” This ensures the amount is clear and reduces the risk of fraud.

How to write a check with thousands and cents:

- $1,234.56 → Write “1,234.56”

- $5,000.00 → Write “5,000.00”

How to write a check with cents:

- $25.75 → Write “25.75”

- $100.50 → Write “100.50”

4. Amount in Words

On the line below the payee’s name. Writing the amount in words eliminates ambiguity, ensuring the amount is clear even if the numbers are wrong. An example would be “One Million dollars.”, or: $1,234.56 → “One thousand two hundred thirty-four and 56/100”

5. The Memo ( optional)

Although optional, the memo section contains the purpose of the payment. This helps in both personal and business record-keeping. When filling out a check, noting “investment” or “Invoice 12345” provides context for the payment.

PS: Clear records also make it easier to understand which expenses may qualify as deductions later, especially when learning what can and cannot be written off.

6. Sign Your Check

The signature line at the bottom right is where you authorize the payment. Sign your name carefully to validate the check. Without a signature, the check is invalid.

Common Mistakes to Avoid When Filling Out a Check

When writing a check, avoiding check-filling errors is crucial for ensuring payment is processed smoothly. Let’s check them out:

1. Wrong Dates

Ensure the date written on the check reflects the current day. An incorrect date can lead to complications with cashing or depositing the check. Remember, checks need to be cashed by the payee within six months, after which they become expired and won’t be honored.

2. Misspelling Payee’s Name

Spelling out the payee’s name ensures the intended recipient can properly cash or deposit the check. Misspellings or omissions can lead to payment delays and disputes.

3. Mismatch in Amounts

The number amount and the written amount must be the same. If they don’t match, the bank may reject the check. That means delays, confusion, and extra work for everyone involved.

4. Missing Signature

Without your signature, the check is useless. Before sending it, do a quick final scan: date, payee, amount, and signature. This 10-second review can save days of payment delays.

To learn how to protect yourself, check out these tips on how to spot and avoid fake check scams from the FTC.

5. Incorrect Check Details

Wrong dates, amounts, or names can slow down payments and confuse your records. The memo line helps you remember why the check was written for example, “Office rent – May” or “Invoice #245.” This makes tracking expenses much easier later.

Recording and Tracking Business Expenses with Checks

Managing business expenses with checks keeps your finances in order. Clear records and regular reconciliations ensure accurate financial statements and prevent errors.

Record your transactions.

Always write down the check number so you can track it later. If a check doesn’t clear, you’ll know exactly which one it is.

Add the date and a short description of the payment. Keep it simple, like “Website hosting” or “Supplier payment.” Then record the amount in the correct column. Updating your balance after each entry helps you avoid overdrafts and surprises

If you ever need guidance or support with your financial management, help is available to ensure everything is in order.

Reconcile Bank Statements Monthly

Match your check register with your monthly bank statements. This ensures all transactions are accurate. If you spot errors or unauthorized charges, address them immediately. Monthly reconciliation keeps your books clear and trustworthy.

Learn more about important tax deadlines to stay organized.

How to Write a Check: Pro Tips

- Use a pen, never pencil

- Don’t leave blank spaces

- Keep your checkbook balanced

- Store checks safely

- Order new checks before running out

Tracking Your Checks

Write down each check in your check register:

- Check number

- Date

- Who you paid

- Amount

- What it was for

Writing Checks for Business Use

1. Can I write a business check to myself?

Yes. You can write a business check to yourself when moving money from your business account to your personal account. Just make sure you record the reason clearly, such as “owner draw” or “reimbursement,” so your tax records stay clean.

2. Are handwritten checks still accepted by banks and vendors?

Most banks and vendors still accept handwritten checks as long as they are filled out correctly and clearly. However, always verify with your vendor or service provider if they prefer electronic payments.

3. What should I do if I make a mistake while writing a check?

If you make a mistake, don’t try to fix it by crossing things out. Instead, write “VOID” across the check, keep it for your records, and write a new check. This avoids confusion and reduces the chance of the bank rejecting it.